Last year, we brought attention to four trends anticipated to impact the Australian start-up community. Let’s evaluate how our predictions fared out.

ClimateTech would be a hot sector for private investors: Correct. CleanTech around the world had an enormous year delivering US $70.1B of invested capital, an 89% increase on 2021 investment levels (US $37B). The sector performed well due to increasing public awareness about the need for sustainable solutions, favourable government policies and incentives, and advancements in technology. We believe this sector will continue to enjoy preferential allocation as investors take longer-term views on technology that will tackle Earth’s biggest challenges. Sprint’s portfolio company, Vapar, continues to kick goals in this arena.

Existing industries would begin to adopt Web 3 & metaverse tech: Accurate. Popular sports, fashion and coffee brands, among other industries, launched web 3 projects in an effort to improve the way they capture and engage with their clients and customers. Among others, these brands included the likes of Nike, Prada, Starbucks, Disney and Reddit. We expect this trend will continue to grow with loyalty emerging as one of the first broad use cases of this technology. With rising customer acquisition costs and the value of repeat customers, more brands will reimagine their loyalty programs with web 3 rails. The adoption of metaverse/VR tech by industries will take more time as the hardware required to support this tech continues to be built.

Food delivery start-ups would innovate how we receive groceries: It was a difficult year for food delivery start-ups as local players, Voly and Send, collapsed. For reference, both of these companies had similar elevator pitches – quick groceries delivered to your doors within 10 to 15 minutes. It was a model that catered mainly to millennials and college students, consumer populations that prioritise convenience over almost every other variable – sometimes even price. However, empirical evidence has shown this model is plagued by serious challenges. Poor unit economics, thin margins, and the logistics infrastructure needed to deliver millions of goods in as little as 15 minutes is extraordinarily complicated. This is not to say grocery delivery as a concept does not have merit or upside. It gives flexibility for caregivers, people with erratic schedules and those with disabilities. And US companies, like GoPuff and FreshDirect, have shown similar services can be offered profitably at a smaller scale. It will be interesting to see how the remaining players innovate and adapt their business models to ensure long-term success.

Deal activity would heat up among local investors: Yes, but.. Australian deal activity fired up at the beginning of the year, with the first quarter recording 219 VC-backed deals and $2.8B of capital invested. This marked a 42% increase in aggregate deal value when referenced against the same period in 2021. Activity quickly tapered off from the second quarter onward as venture investors began scaling back their investment pace. H2 of 2022 saw many funds retreat from larger ticket investments, and refocus on early-stage deals and pre-revenue companies. This is because early-stage companies are typically more isolated from the external factors that affect pre-IPO and public companies.

Thematics for 2023

Now, moving onto three themes for this year:

- AI eats the enterprise / workflow SaaS

- Rise in ambient health monitoring tech

- Challenging year for exits – but a great time to invest

AI eats the enterprise / workflow SaaS:

As a venture firm, we’re always keeping a close eye on the latest and greatest advancements in technology. And right now, the buzzword on everyone’s lips is Generative AI. Released in 2022, this groundbreaking technology is poised to revolutionise the way we live and work, much like the rise of mobile and cloud did over a decade ago.

The past year has seen a flurry of excitement around the next big thing in tech. Virtual reality, autonomous vehicles, crypto, and Web 3 are all promising, but they’re still in their early stages. We believe that Generative AI is at a tipping point more than the former; poised to unleash a wave of innovation unlike anything we’ve seen before.

There are two forces driving this thesis. First, the massive improvements in image and language models which we’ve witnessed. Second, companies like OpenAI, Hugging Face and Stability.ai are beginning to open-source valuable infrastructure. The most well-known right now would be OpenAI’s Chat GPT-3.

These forces are expanding the possibilities of use cases for this technology. Broadly, these use cases will fall into two buckets: enhancing creativity and optimising productivity. One only needs to look at tools like DALL-E and Runway to appreciate how much AI opens the field to non-creatives, and helps to increase creativity. Content creation will explode as AI makes it easier than ever to dream up posts, pictures, movies, etc.

Images created by AI. They were not taken by a camera.

Although we’re more interested in productivity gains this technology will create within the modern workplace. Much of what happens in the modern workplace is just pushing around language; whether that’s legal contacts, code, invoices or email. And if you’ve ever spent a whole day responding to emails, you’ll know the deciphering and exchange of language is slow and unwieldy. To combat this, new enterprise tools are starting to emerge that automate many of these tasks as organisations look to stay ahead of the curve. Take Gong for example – a new tool which helps B2B sales teams be more efficient and effective. We’ve also seen this in GitHub’s CoPilot, which turns natural language prompts into coding suggestions across dozens of programming languages.

The early targets of AI (particularly built on language models) are rote, repetitive tasks within enterprises. Think data entry, data analysis and customer service. Employees will be freed up to focus on more complex and value-adding tasks, and organisations will become more efficient and productive. This year we will see new AI tools propel SaaS into a massive second wave that increases workers’ productivity measurably. Enterprises will swiftly adopt these tools and AI/ML will become a requisite feature in most workflow SaaS solutions. Examples in our portfolios include XBert, Greenlake Medical and Bitwise Agronomy.

Healthcare’s invisibility trick: ambient health monitoring:

Ongoing, passive healthcare monitoring may soon prove the adage that an ounce of prevention is worth a pound of cure.

‘Ambient health monitoring’ systems are taking off. These solutions rely on a broad range of sensors to collect data relevant to patient health – with the goal of offering less intrusive, more practice diagnoses and treatments to improve health outcomes.

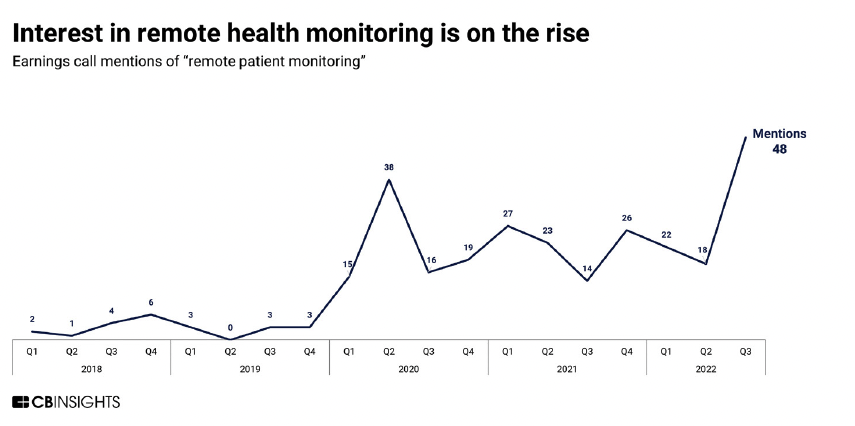

It’s no wonder that this technology is gaining traction, especially with the onset of the global COVID-19 pandemic, which has accelerated the demand for remote patient monitoring (RPM) solutions.

RPM tech captures and analyses patient data in real-time, enabling virtual care and ongoing disease management. This trend has been on the rise since 2020, with earnings transcript mentions of “remote patient monitoring” remaining elevated.

Source: CBInsights

As we move into 2023, RPM tech is set to evolve into a more advanced form. The reliance on wearables will decrease, while the use of passive, ubiquitous sensors will increase. One notable example is Google’s acquisition of Sound Life Sciences, a digital therapeutics startup that offers an FDA-cleared smartphone app. The app leverages sonar technology to monitor breathing patterns, providing a non-invasive way to diagnose sleep apnea and monitor other conditions.

One of our own portfolio companies, Umps Health, is pioneering in this space as well. Their product is an innovative monitoring platform which uses smart plugs to identify abnormalities in an individual’s appliance use that can indicate a decline in wellbeing. This will help caregivers deliver adequate care to older people and people living with a disability. We expect a strong year for Umps as caregivers begin to plan how they will support patients under the Government’s Home Care Package system beginning in 2024.

The success of this tech will rely heavily on the underlying IoT infrastructure that supports fast, accurate communication between devices. Companies eager to make their mark on the space will do well to invest not only in innovating health devices, but also in the AI and connectivity tech that will power them.

Challenging year for exits – but a great time to invest:

This year will be a tough year for VC exits, due to macroeconomic factors and the volatility within financial markets. Despite these challenges, there is reason for plenty of optimism within the early stage component of venture capital.

The horizon for this asset class (7- 10 years) looks beyond the immediate economic turbulence cycle in front of us in 2023 to a more positive future horizon.

As economies slow during 2023 there will be a greater emphasis on operational efficiency and digitalization across industries. Enterprise budgets will shift from growth-driven categories to cost-saving and productivity improvement ones. This will provide a boost to start-ups focused on these areas that build tech-enabled tools.

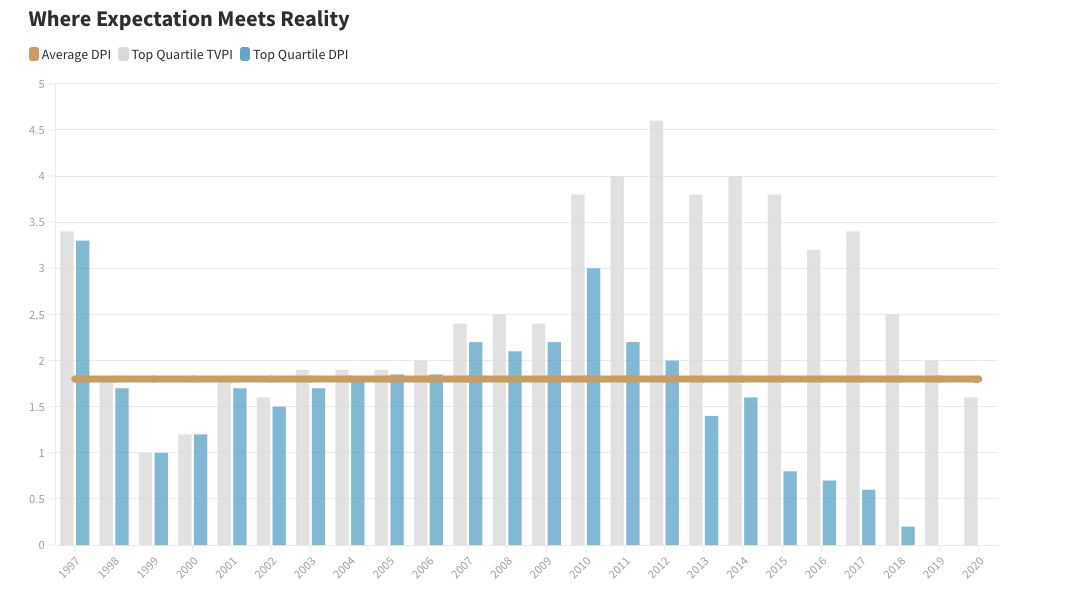

Whilst the cost of financial capital will continue to increase (and the supply decrease), solid startups and scale-ups with great fundamentals will emerge in a tight funding environment. Flat rounds or down rounds will become more common, creating more attractive opportunities for investment. This will be a key ingredient in shaping some of the best performing investment vintages in the years to come. This forecast comes from studying the last 20 years of venture returns data. The highest returning vintages have typically occurred in years following economic turbulence, both in terms of Distributed to Paid-In Capital (DPI) multiples and DPI as a percentage of Total Value to Paid-In Capital (TVPI). They say history tends to repeat itself, and we think the next few years will be no different.

Source: Altimeter Capital

Whilst the outlook ahead remains turbulent, truly great companies will rise (like cream) to the top by capitalising on opportunities presented and executing well.

We plan to participate actively in these opportunities in 2023. We look forward to applying our different forms of capital, including experience, networks and financial, to support the next generation of industry leaders build a better future.

- https://www.holoniq.com/notes/2022-climate-tech-vc-funding-totals-70-1b-up-89-from-37-0b-in-2021

- Preqin [Accessed 1 February 2023]